The IRS has issued a direct deposit update tied to $2,000 payments, with distributions scheduled to begin January 18. This article explains what that update means, who may qualify, the rules that apply, and the precise actions you should take now.

$2,000 IRS Direct Deposit Update: What it means

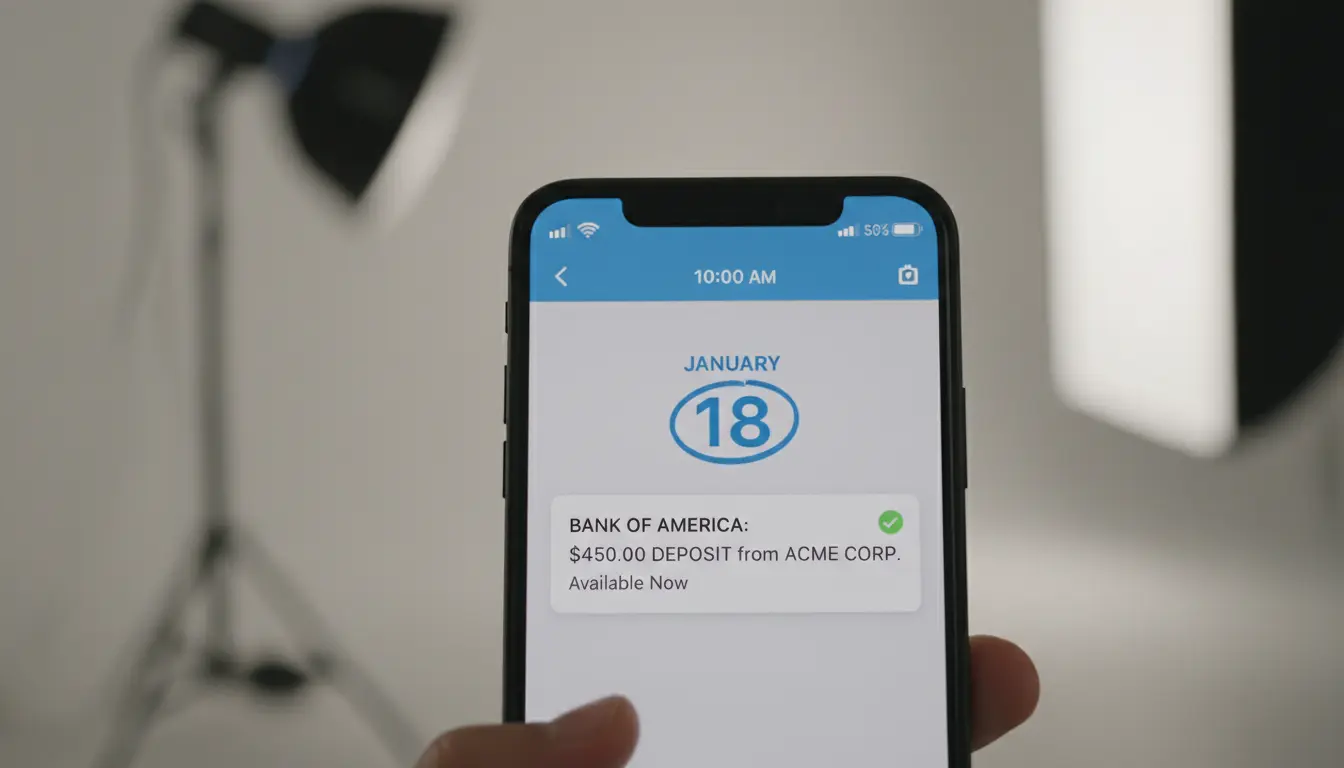

The update signals a new disbursement effort that will use direct deposit where the IRS already has bank account information. Payments are scheduled to start on January 18 for eligible recipients and will continue in phases.

This is not a replacement for existing refunds or benefits. It is a separate payment stream and follows specific eligibility and delivery rules set by the IRS.

Payments Starting January 18: timing and delivery

The IRS will begin direct deposit payments on January 18. Payments are typically released in waves, so not everyone will receive funds on the first day.

- First wave: deposits to accounts on file with the IRS.

- Subsequent waves: payments to recipients with verified identity or after additional processing.

- Alternate delivery: paper checks or prepaid debit cards for those without valid bank details on file.

How the IRS chooses accounts for direct deposit

The IRS uses the most recent bank information it has from tax returns, Social Security payments, or other registration portals. If your account details are missing or flagged, the IRS may issue a paper check instead.

Who qualifies for the $2,000 direct deposit

Eligibility will be defined by IRS guidance for this program. Generally, qualification depends on prior filings, reported income, and other policy details announced by the agency.

Common eligibility factors for these kinds of payments include:

- Filed tax returns for the required tax years or used the IRS non-filer portal if allowed.

- Income thresholds or phase-outs specified by the program rules.

- No disqualifying status such as ineligible dependent status or claim conflicts.

Key rules to know about the direct deposit update

Understanding the rules helps you avoid delays and spot potential problems. Here are the main points to check.

- Bank info: The IRS will use the bank account on file from your most recent tax return or federal payment record.

- Timing: Deposits are made in batches; your bank posting date may vary from the IRS payment date.

- Verification: If additional identity checks are required, your payment may be delayed until verification completes.

- Reconciliation: If you changed banks since your last filing, the payment may be issued by check instead of direct deposit.

What to do immediately: step-by-step actions

Take these steps now to improve your chance of a direct deposit and to protect yourself from delays or fraud.

- Check your IRS online account. Confirm whether the IRS lists a payment status and whether a direct deposit is scheduled.

- Confirm bank details used by the IRS. Compare the account on file to your current account and note discrepancies.

- If you need to update info and the portal allows it, use the official IRS site only. Never share personal details via email or text links.

- Monitor your bank account starting January 18. Watch for deposits, small verification credits, or unexpected holds.

- Keep documentation: save notices, screenshots, and bank statements in case you need to dispute or trace the payment later.

Who to contact if something is wrong

If you don’t receive the payment and expected one, start with the IRS online tools and notices. If the online tools don’t resolve the issue, contact the IRS directly using phone numbers or channels listed on IRS.gov.

Avoid third-party outreach that appears unsolicited. Scammers often mimic IRS notices during payment programs.

Common problems and how to fix them

Problems that block direct deposit are common but often fixable with the right steps.

- Wrong bank account on file: Update your account on the next tax return or consult IRS guidance for interim options.

- Payment returned by bank: The IRS will generally reissue a payment as a paper check to the address on file.

- Identity verification hold: Respond promptly to IRS identity requests using the secure channels indicated in their notices.

Small real-world example

Case study: Maria, a part-time worker, checked her IRS account on January 10 after hearing about the $2,000 update. She discovered her direct deposit on file was an old closed account. She followed these steps:

- Downloaded and saved the IRS notice screen.

- Contacted her bank to confirm the closed account status.

- Informed the IRS via their official portal and prepared to accept a mailed check.

Maria received a paper check two weeks after the initial wave. Because she acted early and kept records, she avoided delay when resolving the returned deposit.

Final checklist before January 18

- Check IRS account and payment status.

- Verify bank account details and mailing address on file.

- Prepare to monitor accounts for deposits starting January 18.

- Keep an eye out for official IRS messages and avoid scams.

Following these steps will reduce the chance of delays and help you respond quickly if a problem arises. If you are unsure about eligibility or see unusual activity, use IRS.gov and official phone lines for next steps.